Interest-free financing is often the first thing people associate with Murabaha. But Murabaha is far more than a simple alternative to conventional lending.

Murabaha replaces a loan with a real sale transaction. Instead of earning interest on money, the financier purchases an asset and resells it at a disclosed profit.

Murabaha also raises important questions:

How does it actually work in practice? Why do many scholars consider it Sharia-compliant? What role do asset ownership and risk play? How is Murabaha used in banking, trade finance, and investment products?

In this guide we explain the applications, benefits, risks, and scholarly debates surrounding Murabaha.

What Is Murabaha in Islamic Finance?

Murabaha is a Sharia-compliant sale contract in which a financier purchases an asset and resells it to a customer at a disclosed profit margin.

Some features distinguish Murabaha from conventional lending:

First, Murabaha is not a loan agreement. The transaction is based on the sale of a real asset rather than the lending of money. The financier earns profit through trade, not through interest charged on borrowed funds.

Second, the asset being sold must be clearly identifiable, legally owned, and capable of being transferred. Murabaha cannot be based on vague, non-existent, or purely notional assets.

Third, the financier must acquire ownership before reselling the asset. During this period, however brief, the financier assumes ownership-related rights and responsibilities. This ownership element is a fundamental part of the contract's structure.

Another requirement is full disclosure. The customer must know the original purchase cost, the agreed markup, the final sale price, and the payment terms. The profit cannot be hidden within complex pricing formulas or undisclosed charges.

The AAOIFI recognizes Murabaha as one of the formal structures within Islamic banking and maintains dedicated standards governing its use.

According to ResearchGate, Islamic finance scholar Taqi Usmani and several industry studies note that Murabaha accounts for a dominant share of Islamic bank financing and is often considered the “default” structure for many banking products. because it solves a problem many people face:

How can financing exist without relying on interest?

How Does a Murabaha Transaction Actually Work?

Murabaha follows a straightforward sequence. The structure usually involves three parties:

Customer

Financier or bank

Supplier or seller

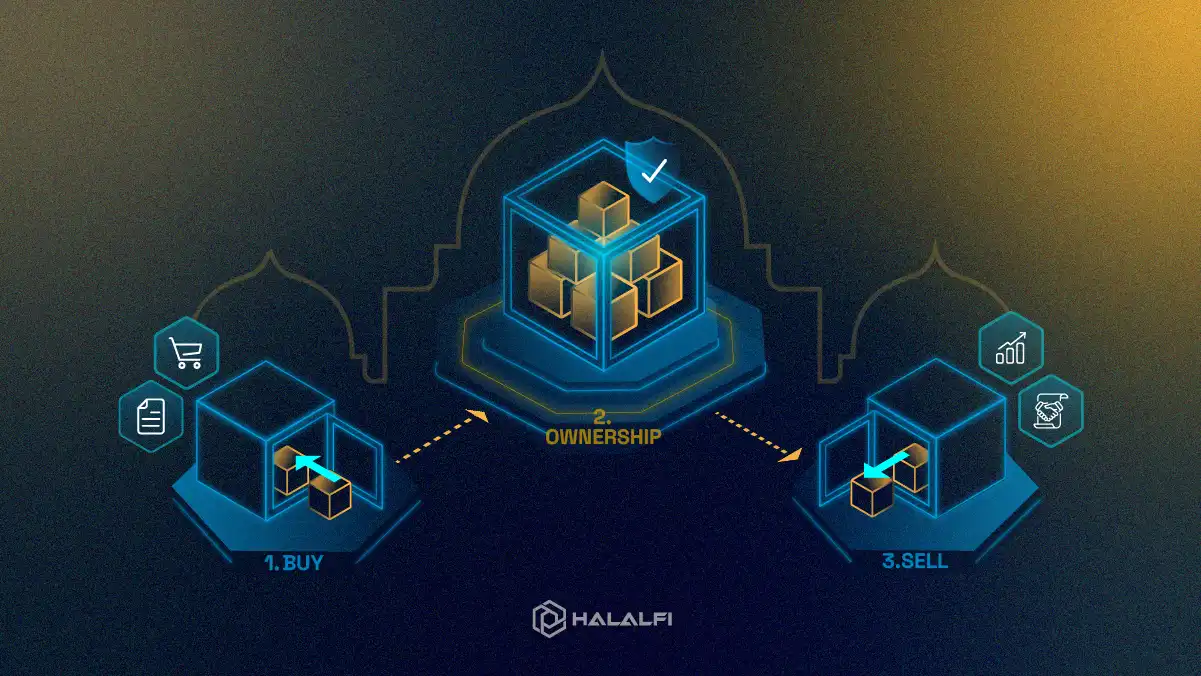

The process looks like this:

How Does a Murabaha Transaction Work?

A Murabaha transaction follows a process designed to ensure that profit will be generated through the sale of a real asset rather than through lending money:

Step 1: Customer Request

The customer identifies an asset. It could be:

A car

Machinery

Inventory

Property

Raw materials

The customer asks the bank or financier to acquire it.

Step 2: Financier Purchases the Asset

The bank purchases the asset from the supplier, and it is essential. The financier must assume ownership before resale.

The ownership risk is one of the main reasons Murabaha differs from conventional lending.

Step 3: The asset is sold to the customer

The bank resells the asset. The final price equals:

Cost + Agreed Profit

Both parties know:

Original cost

Markup

Repayment schedule

Final sale price

There is no hidden pricing, no floating interest, and no surprise adjustments, which helps build trust and confidence in the process for the audience.

Step 4: Payment Through Installments

The customer pays over time. The profit margin is fixed at the outset, typically determined by the asset type, market conditions, and risk factors.

This fixed markup represents commercial profit from trade rather than interest on money, ensuring transparency and predictability for the customer.

Step 5: The Murabaha Sale Is Executed

Only after ownership has been established can the Murabaha sale contract be concluded. At this point, the financier sells the asset to the customer at:

Cost + Agreed Profit Margin

Transparency is essential. The customer must be informed of:

The original purchase cost

The profit markup

The final sale price

Payment terms

Any relevant fees or charges

Unlike conventional interest-based financing, the profit is disclosed as part of the sale transaction rather than calculated as interest on borrowed money.

Step 6: Ownership Transfers to the Customer

Once the Murabaha agreement is executed, ownership of the asset transfers to the customer according to the terms of the contract.

The customer can then use, operate, sell, or benefit from the asset, subject to any contractual conditions that may apply.

Step 7: Payment Takes Place Over Time

The customer repays the agreed sale price according to a predetermined schedule. Payments may be monthly, quarterly, or structured around business cash flows, depending on the arrangement.

Because the profit margin was fixed when the sale occurred, the amount owed does not fluctuate with interest rates after the contract has been completed. Both parties know from the outset:

Total amount payable

Payment dates

Duration of the financing arrangement

A Murabaha Story: Buying a Boat Without Interest

Imagine a small business owner named Bilal. Bilal wants to buy a commercial fishing boat priced at $100,000.

Traditional financing would likely involve a loan with interest tied to the repayment term and market rates.

Under Murabaha, the process changes. The bank buys the boat for $100,000. It then sells the boat to Bilal for $109,000, payable over three years.

Bilal knows the full amount from day one. The bank earns profit through sales, not through lending money at interest.

If the boat were damaged while under bank ownership, the bank would bear that ownership risk.

That temporary ownership risk is an important element of Murabaha. Still, Sharia law also depends on transparent cost disclosure, valid asset transactions, proper contract structure, and the avoidance of interest-based charges. The economics may resemble financing. But the legal and ethical structure differs.

Murabaha vs Conventional Loans

Is Murabaha really different from a loan? The answer becomes clearer through comparison:

Feature | Conventional Loan | Murabaha |

Structure | Lending | Sale contract |

Earnings | Interest | Profit markup |

Asset ownership | The customer buys directly | Financier buys first |

Asset backing | Not required | Required |

Pricing | Interest-based | Fixed sale price |

Sharia status | Often involves RIBA | Generally halal |

The cash flows of a Murabaha transaction can sometimes resemble those of a conventional loan.

In both cases, the customer acquires an asset and repays a higher amount over time through scheduled installments. The differenece, lies in the legal and commercial structure.

A conventional loan is based on lending money and charging interest, whereas Murabaha is based on the purchase and resale of a real asset at a disclosed profit.

Riba in Islam is not merely about increasing money. It concerns guaranteed gain disconnected from real economic participation. Murabaha seeks to link financing to trade.

Why Is Murabaha Considered Halal?

Islamic law prohibits riba, usually understood as unjustified or predetermined gain generated from lending money.

The Qur’an at Surah Al-Baqarah, verse 275 (2:275) states:

“Allah has permitted trade and forbidden interest.”

ٱلَّذِينَ يَأْكُلُونَ ٱلرِّبَوٰا۟ لَا يَقُومُونَ إِلَّا كَمَا يَقُومُ ٱلَّذِى يَتَخَبَّطُهُ ٱلشَّيْطَـٰنُ مِنَ ٱلْمَسِّ ۚ ذَٰلِكَ بِأَنَّهُمْ قَالُوٓا۟ إِنَّمَا ٱلْبَيْعُ مِثْلُ ٱلرِّبَوٰا۟ ۗ وَأَحَلَّ ٱللَّهُ ٱلْبَيْعَ وَحَرَّمَ ٱلرِّبَوٰا۟ ۚ فَمَن جَآءَهُۥ مَوْعِظَةٌۭ مِّن رَّبِّهِۦ فَٱنتَهَىٰ فَلَهُۥ مَا سَلَفَ وَأَمْرُهُۥٓ إِلَى ٱللَّهِ ۖ وَمَنْ عَادَ فَأُو۟لَـٰٓئِكَ أَصْحَـٰبُ ٱلنَّارِ ۖ هُمْ فِيهَا خَـٰلِدُونَ

Trade is allowed, and Interest is prohibited. Murabaha, therefore,e becomes permissible because profit emerges from commercial sale rather than money lending alone.

Some critics argue that Murabaha yields outcomes similar to conventional lending, but the ownership risk and asset transfer create real commercial exposure, fostering a sense of fairness and shared risk.

The debate remains active. But AAOIFI standards and Islamic banking practice generally recognize Murabaha as halal when structured correctly.

Conditions for a Sharia-Compliant Murabaha

According to the conditions outlined in AAOIFI Shariah Standard No. 8, a Murabaha transaction should satisfy some core requirements:

The underlying asset must be identified, lawful, and capable of ownership and transfer.

The financier must purchase and own the asset before selling it to the customer.

The financier must assume ownership-related risk and liability during the period of ownership.

The customer cannot purchase the asset on behalf of the financier unless a valid agency (wakalah) arrangement exists.

The original acquisition cost must be disclosed to the customer.

The profit markup must be clearly disclosed and agreed upon.

The Murabaha sale contract must be executed only after the financier has acquired ownership or constructive possession of the asset.

The sale price and payment schedule must be known and fixed at the time of contracting.

The transaction must not involve riba (interest), excessive uncertainty (gharar), or prohibited assets.

Any late-payment provisions must comply with Sharia requirements and cannot function as interest charges.

The transaction should represent a genuine sale of an asset, not merely a mechanism for advancing cash.

Murabaha Risks and Default: Is Murabaha Completely Risk-Free?

Murabaha is often viewed as one of the safer forms of Islamic financing. But “safer” does not mean risk-free. Every financing structure carries risk.

Murabaha distributes risk differently. Many people assume Islamic finance eliminates uncertainty. It does not; Islamic finance aims to manage uncertainty fairly.

That concern connects with gharar in Islamic finance, which refers to excessive ambiguity or unclear contractual terms. Murabaha reduces gharar through transparency. The customer knows:

Asset cost

Bank markup

Payment schedule

Ownership transfer conditions

Total repayment amount

Nothing is hidden, yet risk still exists. The primary Murabaha risks include:

Customer default

Asset damage during ownership

Documentation errors

Operational failures

Counterparty payment risk

Sharia Compliance Challenges

Documentation and Contractual Issues

Ownership and Asset Transfer Concerns

Delivery and Asset Performance Delays

Benchmark Pricing Concerns

Customer Default Risk

Operational Failures

Commodity Murabaha Implementation Risks

Contractual Disputes

Regulatory and Legal Uncertainty

But these are commercial risks, not speculative risks.

What Happens If Someone Defaults on a Murabaha Contract?

Murabaha default creates a unique challenge. In conventional lending, missed payments often trigger compounding interest or late-payment penalties. Murabaha works differently.

Islamic banks generally cannot increase repayment through additional interest after default. It creates tension.

The financier still faces financial loss. But Islamic principles prohibit turning hardship into a profit center.

The Qur’an at Surah Al-Baqarah (2:280) states:

“If the debtor is in difficulty, grant him time until it is easy for him to repay.”

وَإِن كَانَ ذُو عُسْرَةٍ فَنَظِرَةٌ إِلَىٰ مَيْسَرَةٍ ۚ وَأَن تَصَدَّقُوا خَيْرٌ لَّكُمْ ۖ إِن كُنتُمْ تَعْلَمُونَ

This principle influences Islamic banking practice.

Genuine hardship may justify restructuring or delay, and Willful default is treated differently. Many Islamic institutions distinguish between:

Genuine Hardship

Her repayment difficulty is real and unavoidable. Examples:

Business collapse

Medical hardship

Severe economic disruption

Willful Default

He is intentionally delaying repayment despite the ability to pay. Islamic banks often consider this misconduct. Some institutions use:

Legal enforcement

Security realization

Customer blacklisting

Court recovery

Because Murabaha cannot rely on punitive interest, institutions continue developing alternative approaches to discourage abuse.

Why Genuine Ownership Matters in Murabaha?

In Murabaha that ownership must be genuine rather than merely symbolic. The financier cannot simply provide funds and label the transaction a sale. It must acquire ownership of the asset before selling it to the customer.

This ownership carries legal and commercial consequences. During the period in which the financier owns the asset, it also bears the responsibilities and liabilities associated with ownership. Even if this period is brief, the ownership must be real enough to transfer both rights and risks.

For example, if an asset is damaged, destroyed, or becomes defective before it is resold to the customer, the loss generally falls on the party that owns the asset at that time. If the financier is still the owner, the financier bears that risk rather than the customer.

This principle reflects a broader concept in Islamic finance: profit should be linked to ownership, risk, and commercial activity. A party should not earn a return without first accepting some degree of responsibility connected to the underlying asset.

The issue becomes important when distinguishing Murabaha from conventional lending. If a bank simply advances money to a customer and never acquires the asset itself, the transaction begins to resemble a traditional loan.

In that situation, the financier earns a return without participating in ownership or trade, which undermines one of the key foundations of Murabaha.

For this reason, it is important to examine whether ownership was genuinely transferred, whether the financier assumed ownership-related liabilities, and whether the transaction involved a real sale rather than merely replicating the economic effect of a loan.

Is Murabaha Just Disguised Interest?

You can see the question in forums, finance discussions, and even among Muslims exploring Islamic banking for the first time. The criticism usually sounds like this:

“The customer pays more than the original price. Isn’t that basically interesting?”

The concern is normal. The economic outcome can appear similar. But Islamic finance focuses heavily on structure and legal form.

Murabaha is not structured as:

Money → Interest → Repayment

Instead, it follows:

Asset → Ownership → Sale → Profit

That sequence matters.

Profit comes from commercial sales, not from automatically generating money. Some economists still debate whether Murabaha dominates Islamic finance too heavily.

Islamic finance author Harris Irfan, in the book "Heaven’s Bankers," says:

“Murabaha has become the single most common method of funding in Islamic finance.”

His observation reflects reality.

Murabaha is practical, perhaps too practical. Some scholars argue that Islamic finance originally emphasized partnership structures such as musharakah and profit-sharing more strongly than debt-like financing.

Red Flags in Murabaha Structures

Murabaha is accepted within Islamic finance, but one concern arises when the financier never genuinely acquires ownership of the asset.

If the institution simply provides funds while the customer purchases the asset directly, the arrangement can begin to resemble conventional lending rather than a true sale transaction.

When contracts are purely formalities and no meaningful commercial responsibility is assumed by the financier, the economic substance of the transaction may differ from its legal description.

Pricing practices can create further debate. While using conventional market benchmarks to determine Murabaha profit margins, the markup merely mirrors an interest rate without any clear connection to the underlying trade transaction.

Commodity Murabaha remains another area of discussion. Some view it as a practical tool for liquidity management and investment products.

Others, however, argue that certain implementations function primarily as cash financing disguised as commodity trades, particularly when the commodities have little commercial significance beyond facilitating the movement of funds.

Transparency is important. Murabaha is built on disclosure, meaning customers should clearly understand the purchase cost, profit margin, payment obligations, fees, and contractual terms.

When disclosures are incomplete or difficult to verify, the transaction may fall short of the transparency standards that Murabaha is intended to uphold.

How Murabaha Compares to Other Financing Models?

Murabaha is only one part of Islamic finance. Understanding the alternatives helps people choose more intelligently. Let's see the comparison:

Feature | Conventional Loan | Murabaha | Ijarah | Musharakah | Mudarabah |

Structure | Loan | Cost-plus sale | Lease | Partnership | Profit-sharing partnership |

Bank/Financier Income | Interest | Disclosed profit markup | Rental payments | Share of profit | Share of profit |

Asset Ownership | Customer | Financier first, then customer | Financier during lease term | Shared ownership | Typically owned by the venture/business |

Risk Exposure | Mostly transferred to borrower | Ownership risk before resale | Ownership and asset-related risk during lease | Shared according to participation | Capital provider bears financial loss; manager bears performance risk |

Return Certainty | Usually fixed | Usually fixed after sale | Usually predetermined rent | Variable | Variable |

Profit/Loss Sharing | No | No | No | Yes | Yes |

Suitable For | General borrowing | Asset purchases and trade finance | Equipment, vehicles, property leasing | Joint ventures and business ownership | Investment and business management arrangements |

Flexibility | High | Moderate | Moderate | High | High |

Sharia Status | Often problematic due to riba | Generally accepted when properly structured | Generally accepted when properly structured | Often viewed as closely aligned with Islamic finance principles | Often viewed as closely aligned with Islamic finance principles |

Musharakah deserves special attention. Unlike Murabaha, Musharakah involves partnership. Both parties contribute capital and share outcomes. It creates stronger alignment between the financier and entrepreneur.

Many scholars see Musharakah as closer to the original spirit of Islamic finance because it emphasizes participation rather than debt-like repayment.

Murabaha remains dominant because it offers predictability, and Musharakah offers a deeper partnership. Both serve different purposes.

What Is a Murabaha Deposit?

Murabaha is not limited to financing; it also supports halal investment and treasury solutions. In Murabaha deposits, returns are generated through real trade rather than interest, with institutions often acting as agents (wakalah) on behalf of investors.

Money is not simply deposited to earn interest. Instead, the customer typically appoints the institution through wakalah, an agency arrangement, to conduct Sharia-compliant trade. The process often follows this cycle:

1. Agency Appointment (Wakalah)

The depositor authorizes the institution. This is the wakalah stage. The institution acts as an agent.

2. Asset Purchase

The bank purchases approved commodities or assets. Often these involve metals traded through recognized commodity markets.

3. Cost-Plus Sale

The commodity is resold. Profit is generated through trade, not lending.

4. Customer Receives Profit

At maturity, the customer receives:

Original capital

Agreed profit generated from trade

It creates an Islamic savings structure built on commercial activity rather than interest.

What Is Commodity Murabaha?

Commodity Murabaha is a form of Murabaha that uses readily tradable commodities to facilitate Sharia-compliant investment and liquidity management.

The commodity is not the investment objective; it serves as the underlying asset that enables a genuine sale.

Does the Depositor Actually Buy the Commodity?

In most structures, legal ownership of the commodity passes through the customer, at least contractually.

However, the customer rarely takes physical possession of the commodity. Instead, the institution typically executes the purchase and resale process under the authority granted through wakalah.

Why Is Wakalah Important?

Wakalah allows the institution to act as the customer's agent throughout the transaction process. Without this agency relationship, customers would need to execute multiple commodity trades themselves, which would be impractical for most retail investors.

The wakalah arrangement, therefore, helps make the structure operational while preserving the underlying contractual framework required by Islamic finance.

Why Do Many Scholars Approve Commodity Murabaha?

Supporters argue that Commodity Murabaha satisfies key Sharia requirements because:

Transactions involve identifiable assets.

Profit arises from trade rather than lending.

Contract terms are transparent and disclosed in advance.

The structure avoids conventional interest (riba).

Critics argue that some implementations can become highly standardized and economically resemble conventional fixed-income deposits.

They question whether commodity transactions always represent meaningful commercial activity or merely serve as a legal mechanism to replicate the outcomes of interest-bearing products.

Some scholars, therefore, prefer alternative structures that involve greater participation in business risk and productive investment.

Muhammad Taqi Usmani, while acknowledging that Murabaha is necessary in some cases, has repeatedly warned that excessive reliance on Commodity Murabaha can move Islamic finance away from genuine risk-sharing and entrepreneurship. He argues it should not dominate the industry.

Is the Return Guaranteed?

In a properly structured Murabaha transaction, the profit from the sale is generally fixed and known in advance once the trade is completed. However, this differs conceptually from a guaranteed interest payment on a loan.

The customer's return comes from an agreed sale profit embedded in the Murabaha contract rather than from lending money at a predetermined interest rate. Nevertheless, institutions must clearly explain the nature of the return and any associated risks.

What Disclosures Should Investors Receive?

Good requires clear disclosure of:

The underlying transaction structure.

The role of wakalah and agency arrangements.

The assets or commodities being used.

How profit is calculated.

Any fees and operational costs.

Counterparty and operational risks.

Whether returns are fixed sale profits or projected returns.

The extent of capital protection, if any.

Murabaha Deposits vs Conventional Savings Accounts

The difference becomes clearer through comparison:

Feature | Conventional Savings | Murabaha Deposit |

Relationship | Debtor–Creditor | Buyer–Seller |

Earnings | Interest | Trade profit |

Asset backing | None | Yes |

Basis | Lending | Sale |

Sharia compliance | Often no | Yes |

So Murabaha deposits are frequently promoted as Shariah-compliant investments and alternatives to interest-bearing savings. They remain among the most popular Islamic banking products globally.

Murabaha Around the World: Where Is It Used Most?

Murabaha powers major segments of modern banking. And global adoption keeps growing.

The LSEG Islamic Finance Development Report 2025 ranks Malaysia, Saudi Arabia, and the UAE among the world’s leading Islamic finance ecosystems.

Saudi Arabia remains the largest Islamic banking jurisdiction by scale. Its Sharia banking sector represents roughly 75% of domestic banking assets and roughly one-third of global Islamic banking assets.

Malaysia continues to lead through regulation, education, and product innovation. The country pioneered Islamic banking infrastructure and remains one of the most sophisticated markets globally.

The UAE has become a regional hub. Research places the UAE among the top contributors to global Islamic banking assets.

Pakistan is also growing rapidly. According to the State Bank of Pakistan, Islamic banking assets exceeded PKR 14 trillion by late 2025, reflecting strong expansion.

Sp Murabaha is not niche; it is financial infrastructure.

Murabaha for Businesses: Why SMEs Use It

Murabaha is used by businesses, especially SMEs that need equipment, inventory, or trade financing without giving away ownership. This is because many small businesses face a difficult choice. They either:

Take conventional debt

Give away equity

Or delay growth entirely

Murabaha offers a third route. Instead of lending money directly, the financier purchases the required asset and sells it to the business with a disclosed markup. This structure works well for:

Machinery

Vehicles

Manufacturing equipment

Inventory

Import–export transactions

Trade finance

Murabaha has become one of the most widely used commercial financing tools across Islamic banking.

Murabaha Checklist for SMEs

Before entering a Murabaha agreement, small and medium-sized businesses should evaluate this factors:

Is the asset clearly identified and suitable for a Murabaha transaction?

Has the financier agreed to purchase and own the asset before resale?

Are the original cost and profit markup fully disclosed?

Is the total amount payable clearly stated in the contract?

Does the payment schedule align with the company's expected cash flow?

Are there any additional fees, administrative charges, or penalties?

Who bears the risk if the asset is damaged before ownership transfers?

Are delivery, warranty, and maintenance responsibilities clearly defined?

Does the transaction comply with the business's Sharia requirements and internal policies?

Would another structure, such as Ijarah, Musharakah, or Mudarabah, better suit the business objective?

A Business Story: Growth Without Giving Away Ownership

Imagine a small food-processing company. Demand is growing, and orders are increasing.

The company needs new packaging machinery worth £250,000. Conventional finance is available. But the founders dislike two things:

Variable interest exposure

Giving away equity to investors

Murabaha creates another path. The Islamic financier purchases the machinery. It then resells the equipment to the company with a fixed markup and an agreed installment schedule.

The company receives:

Immediate operational capacity

Predictable payments

No ownership dilution

The financier receives:

Profit from trade

Security over the equipment

Commercial exposure through ownership

The outcome matters, and business grows. But without stepping into structures, it is considered problematic.

Import Murabaha and Trade Finance

Murabaha is common in international trade. Importers frequently need short-term financing to buy inventory before revenue arrives. Letters of credit structured through Murabaha solve this problem.

What is an Import Murabaha?

Import Murabaha is a trade finance arrangement in which an Islamic bank purchases goods from an overseas supplier and then resells them to the importer at a disclosed markup.

Instead of lending money to the importer, the bank participates in the transaction as the owner and seller of the goods.

How does the process work?

The process usually works like this:

1. Importer Needs Goods

The importer selects the products to be purchased. These may include:

Consumer electronics

Industrial equipment

Raw materials

Retail inventory

Agricultural products

The supplier provides a quotation or supplier invoice detailing the goods, quantity, specifications, and purchase price.

2. Bank Purchases the Goods

Using the supplier invoice as a reference, the bank purchases the goods from the supplier.

At this stage, the bank must acquire ownership of the goods before reselling them to the customer.

Depending on the transaction structure, ownership may be evidenced through shipping documents, warehouse receipts, bills of lading, or other documents of title.

Documents of title help demonstrate legal ownership and control over the goods. In international trade, physical possession is often impractical because goods may be in transit across countries or stored in ports and warehouses.

As a result, ownership is frequently established through documentation rather than direct physical possession. These documents play an important role in supporting the validity of the Murabaha transaction.

3. Murabaha Sale to Importer

After ownership has passed to the bank, the goods are sold to the importer under a Murabaha contract.

The agreement clearly discloses:

Original purchase cost

Agreed profit margin

Final sale price

Payment schedule

The importer defers payment, allowing time to sell the inventory before completing repayment.

4. Importer Repays Through Revenue

The importer sells the inventory and uses the proceeds to repay. This system lowers uncertainty while maintaining trade-based financing.

And that matters because Islamic finance discourages financing detached from economic activity.

The World Bank describes Islamic finance as:

“Asset-backed, ethical and risk-sharing finance connected to the real economy.”

When Does the Bank Actually Own the Goods?

The bank must acquire ownership before entering into the Murabaha sale with the customer. The exact moment ownership transfers depends on the purchase contract, shipping terms, and trade documentation.

If the bank merely finances the purchase without genuinely acquiring ownership rights, many scholars would argue that the transaction risks resembling a conventional loan rather than a valid sale.

Risks in Import Murabaha

Murabaha is not risk-free. Risks include:

Shipment delays that disrupt delivery schedules.

Damaged or defective goods during transit.

Foreign exchange (FX) risk occurs when transactions involve multiple currencies.

Counterparty risk if either the supplier or customer fails to perform contractual obligations.

Documentation errors affecting ownership transfer or customs clearance.

Market risk is if the value of goods changes before resale.

The extent to which the bank or the customer bears these risks depends on the contractual structure and the stage of the transaction.

Murabaha and Speculation

Modern finance can involve speculative activities that resemble gambling, making the maysir in Islamic finance relevant.

Many Islamic scholars discourage excessive leverage, casino-style trading, certain derivatives, and highly speculative token trading because they often lack real value creation.

Instead, Islamic finance promotes transactions linked to tangible assets, ownership, trade, and productive economic activity.

Through principles such as the prohibition of riba, limits on gharar, and avoidance of maysir, Islamic finance seeks stronger connections to the real economy.

Murabaha vs Speculative Finance

The difference becomes easier to see visually:

Feature | Speculative Markets | Murabaha |

Value source | Price movement | Trade |

Asset ownership | Often absent | Required |

Earnings | Market swings | Markup |

Transparency | Mixed | High |

Economic link | Sometimes weak | Strong |

Sharia alignment | Often debated | Established |

This does not mean innovation is prohibited. Islamic finance has always evolved. The question is:

What incentives does the structure create?

Murabaha, Islamic Finance, and the Future of Ethical Capital

Murabaha enables financing without relying on conventional interest. It supports homes, businesses, machinery, and international trade. And despite ongoing debates, it continues to serve as a cornerstone of modern Islamic banking.

Yet Murabaha also reveals something bigger. People rarely seek financing alone. They seek:

Stability

Fairness

Trust

Meaningful growth

That broader need is shaping the next generation of finance.

Islamic finance is evolving, and technology is becoming part of that story. Platforms such as HalalFi represent one possible direction.

Not because they promise easy wealth. But because they attempt to reconnect finance with:

Accountability

Transparency

Participation

Real economic value

Is HalalFi a Replacement for Murabaha?

Murabaha solves an important financing problem. But modern finance presents a broader challenge.

People are also asking:

How do I invest ethically? Or how do I support real businesses rather than speculation?

HalalFi is designed as a halal crowdfunding infrastructure. It connects investors with real businesses using blockchain transparency, smart contracts, and business verification rather than relying on hype-driven finance.

The platform focuses on:

Real businesses

Real revenue

Transparent contracts

Performance-based participation

Structured risk mitigation

The idea is not to replace Murabaha. It is to address a different layer of the market. Murabaha finances purchases, HalalFi attempts to finance growth.

Conclusion

Murabaha is sometimes dismissed as technical paperwork.

Murabaha asks a simple question:

Should profit come from lending money alone, or from participating in real economic activity?

Islamic finance answers that question through trade, ownership, and structured risk. Murabaha is one expression of that philosophy.And HalalFi Whitepaper says it attempts to carry those ideas into newer financial environments.

If ethical growth, transparent finance, and business-backed participation matter to you, exploring HalalFi’s model and reviewing its approach to crowdfunding and verification may be a practical next step.

Frequently Asked Questions

Can Murabaha be used for home financing?

Yes. Murabaha is commonly used for home purchases in Islamic banking. The financier buys the property and resells it to the customer at a disclosed markup with scheduled payments.

Does Murabaha always have a fixed profit?

Usually yes. The profit margin is normally agreed in advance, creating predictable repayment obligations.

Is Murabaha available outside Muslim countries?

Yes. Murabaha products are offered in countries including the UK, Bahrain, Malaysia, UAE, and Saudi Arabia through Islamic banks and financial institutions.

Can Murabaha be combined with other Islamic finance contracts?

Yes. Some structures combine Murabaha with wakalah, guarantees, or treasury mechanisms depending on commercial needs.

Why do some scholars prefer Musharakah over Murabaha?

Because musharakah emphasizes direct partnership and shared commercial outcomes rather than fixed-markup financing.

Does Murabaha remove all investment risk?

No. Murabaha reduces certain uncertainties but still involves counterparty and operational risks.

Is commodity Murabaha controversial?

Sometimes. Some scholars accept it as practical and Sharia-compliant, while others argue that it can become overly technical or economically too similar to conventional lending.