What if the money you’re earning every month looks fine on paper… but doesn’t sit right in your heart?

That quiet question has been getting louder lately. Between credit cards, mortgages, “easy” investment apps, and constant financial pressure, it’s becoming harder to tell what’s truly halal and what quietly crosses the line into riba. And the truth is, most people aren’t looking for shortcuts. They just want clarity.

This is exactly where understanding Riba in Islam becomes real rather than theoretical. It’s not just a concept discussed in books; it’s something that shapes everyday decisions, how you save, borrow, invest, and grow your wealth.

In this article, we will discuss Riba, why interest is forbidden, and how to grow wealth without compromising your faith. We also show how HalalFi helps you invest in genuine businesses, earn through shared success, and build wealth with clarity, purpose, and peace of mind.

What Is Riba in Islam?

Riba refers to any guaranteed increase in the amount of a loan or other debt. But here’s the thing, it’s not just about “interest” in the modern sense.

In classical Islamic scholarship, riba includes:

Any predetermined profit on loans

Exploitative financial practices

Unequal exchanges in certain trades

Types of Riba in Islam

Understanding the types helps clarify the concept:

Type of Riba | Description | Example |

Riba al-Nasi’ah | Increase due to delayed payment | Bank loan interest |

Riba al-Fadl | Unequal exchange of similar goods | Trading gold of unequal weight |

Even today, scholars emphasise that most conventional banking interest falls under the category of riba al-nasi’ah.

This is the most common form today. It happens when an extra payment is required because time passes on a loan or debt. Let's see examples based on Academy Musaffa:

1. Riba al-Nasi’ah (Interest due to delay)

Bank loan interest: You borrow €10,000 from a bank. You must repay €11,000 after one year. The extra €1,000 is charged only because of the time.

Credit card debt: You spend €1,000 on a credit card but don’t pay on time. The bank adds interest monthly (e.g., 18–25% APR) until you repay the loan.

Mortgage loans: A home loan of €200,000 becomes €300,000+ over 20–30 years due to interest payments.

2. Riba al-Fadl (Unequal exchange of similar goods)

This happens in trade/barter, not loans. It refers to exchanging the same type of commodity in an unfair way (more for less, or with a different quality, without the rules of fairness). Let's see some examples based on Islamic fiqh:

Gold trading: You exchange 100g of gold for 120g of gold in a direct swap. Even if both are gold, the unequal amount makes it Riba.

Currency exchange in a delayed deal: You agree to exchange €1,000 for $1,100, but delivery happens later.

Why Is Interest Forbidden in Islam?

It’s not just a rule; it’s rooted in both ethics and economic logic. Let's see how:

1. Ethical Perspective

At its core, RIBA challenges fairness. Earning from someone’s hardship, without sharing their risk, creates an imbalance.

Islam promotes compassion and responsibility, where financial dealings should be just, not one-sided. Wealth, in this sense, isn’t just about gain; it’s about how that gain is made.

2. Economic Perspective

From an economic angle, interest shifts all risk to the borrower while guaranteeing profit to the lender. This can widen inequality and create fragile, debt-driven systems.

Islamic finance, by contrast, encourages risk-sharing and real economic activity, which tends to foster more stable, grounded financial growth over time.

A report from the Islamic Financial Services Board (IFSB) noted that countries with stronger Islamic finance principles showed greater resilience to inflation shocks than purely interest-based systems. That’s not just theology, that’s economic reality.

Is Bank Interest Haram in Islam?

Let’s address the question most people are actually asking.

Yes, according to the majority of scholars, bank interest is haram in Islam. But real life isn’t always black-and-white.

According to AIBIM in Malaysia, over 63% of banking assets are now Shariah-compliant.

LSEG reports show that in Saudi Arabia, Islamic banking dominates more than 70% of total financial assets

The banker noted that in Pakistan, the government aims for 100% Islamic banking by 2027

These numbers show a global shift: Muslims aren’t just avoiding riba, they’re building alternatives.

Still, many people remain stuck in conventional systems due to limited access or awareness.

Related Article: Shariah Compliant Investments

What is the interest in Islamic Banking?

Here’s where things get interesting. Islamic banking doesn’t eliminate profit; it changes how profit is generated.

Instead of interest, it uses:

Murabaha (cost-plus financing)

Mudarabah (profit-sharing partnerships)

Ijara (leasing models)

So instead of lending money for profit, banks invest in real assets, share risks with clients and earn through trade or partnership.

This aligns with Sharia law in finance, ensuring ethical and transparent transactions.

How to Avoid Interest in Islam

Avoiding Riba today isn’t always easy, but it’s definitely possible. Here’s what people are actually doing:

1. Switch to Islamic Banks or Windows

Countries like the UAE and Malaysia now offer fully digital Islamic banking options.

2. Use Halal Investment Platforms

The rise of Islamic fintech has made it easier than ever to invest without riba.

3. Explore Crowdfunding Models

Many Muslims are now using Crowdfunding platforms structured on profit-sharing instead of interest.

4. Focus on Asset-Based Financing

Think real estate partnerships, business investments, or trade-based profits.

5. Understand Risk Factors

Avoid gharar in Islamic finance (uncertainty) and mysir in Islamic finance (gambling), which often accompany speculative markets.

What to Do With Interest Money in Islam?

This is a question many people ask quietly. Maybe you inherited it. Maybe you didn’t realise before.

You cannot keep or benefit from riba income. So what should you do?

Give it away to charity (without intention of reward)

Use it for public benefit (e.g., infrastructure, aid)

Do not use it for personal gain

This isn’t about “earning reward”, it’s about purifying wealth.

Where and How to Spend Interest Money in Islam

Let’s be more practical.

Acceptable Uses:

Public welfare projects

Helping people experiencing poverty (without the intention of sadaqah reward)

Emergency community needs

Not Allowed:

Personal use

Family benefit

Religious acts expecting reward

It’s a subtle but important distinction.

Sahih Muslim in the Musaqah says:

لَعَنَ رَسُولُ اللَّهِ ﷺ آكِلَ الرِّبَا وَمُؤْكِلَهُ وَكَاتِبَهُ وَشَاهِدَيْهِ

Imam Ja’far al-Sadiq says:

الرِّبَا أَشَدُّ مِنَ الزِّنَا

Halal Investment vs Riba-Based Finance

Here’s a look at comparing halal investment and riba-Based Finance:

Feature | Halal Investment | Riba-Based Finance |

Profit Source | Trade & risk-sharing | Fixed interest |

Risk | Shared | The borrower bears most |

Ethics | Aligned with Sharia | Profit-focused |

Stability | Asset-backed | Debt-driven |

Compliance | Requires shariah audit | No religious framework |

This is why many investors now prefer ethical investment models rooted in Islamic finance.

How People Are Navigating Riba Today?

Consider someone who shifted from bank loans to equity-based funding. Through Sharia-compliant finance, he raised capital without incurring debt and strengthened relationships with investors.

Another example is someone who started small with halal investment options via a mobile app. Today, his portfolio includes sukuk and ethical stocks.

These people, after leaving conventional banking, now work in Shariah audit, helping institutions ensure compliance.

Expert Insight: A Perspective Worth Reflecting On

Dr Zamir Iqbal, World Bank Islamic Finance Specialist, says:

“Islamic finance is not just about avoiding riba, it’s about building an economy rooted in fairness, transparency, and shared prosperity.”

Common Mistakes People Make About Riba

Let’s clear a few misconceptions:

“Small interest is okay”. No, it’s still RIBA

“Only excessive interest is forbidden”. It is not true

“Islamic banking is just rebranded interest”. No, It is Oversimplification

Understanding the structure matters more than the label.

How Businesses Are Adapting to Riba-Free Models

Businesses are increasingly:

Using principal-protected investment strategies

Offering profit-sharing instead of fixed returns

Partnering with Islamic fintech platforms

Even global firms are exploring Sharia-compliant finance to tap into Muslim markets.

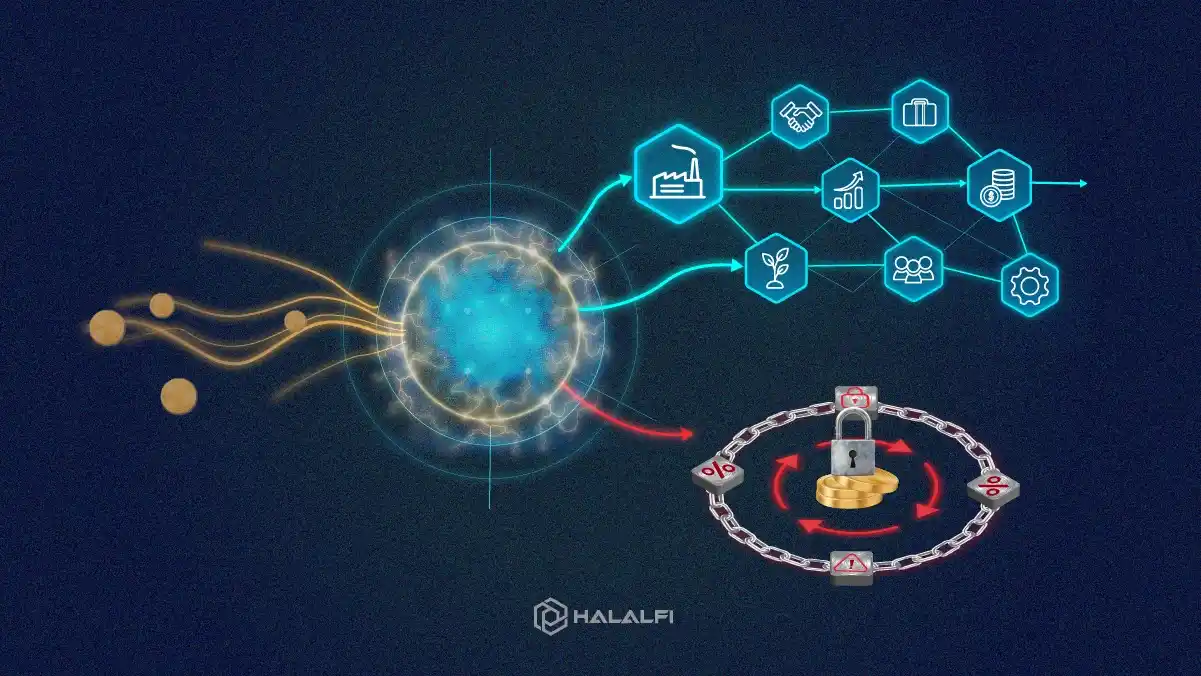

How does HalalFi help make sure our earnings are not based on usury?

In conventional finance, the structure is simple: you lend money, a fixed return is promised, and the profit is generated regardless of the business's actual performance.

In Islamic finance thinking, this creates discomfort because it separates money from real economic activity. Instead, modern Islamic fintech models try to link capital with actual trade, services, or business outcomes.

Instead of fixed interest, some Islamic fintech platforms, such as HalalFi, work by connecting investors with real businesses that need growth funding.

The idea is not about guaranteed returns, but about shared outcomes based on how the business performs. This shifts the model closer to participation rather than passive lending.

This approach reflects a broader principle in Islamic finance: money should be tied to real activity. Rather than “money generating money automatically,” the focus shifts to partnerships in which profit is tied to effort, performance, and risk-sharing on both sides.

From a structural perspective, platforms like HalalFi exemplify how Islamic fintech is operationalising these principles in modern digital environments.

They are not the only model, but they illustrate how technology is being used to reduce dependency on interest-based systems.

Screening, Transparency, and Reducing Financial Uncertainty

One of the concerns in Islamic finance is not only riba, but also excessive uncertainty and speculative behaviour.

Many investors today face products that are difficult to understand, especially in fast-moving digital markets like crypto or unregulated investments.

Some Islamic fintech platforms attempt to address this by adding review layers before listing investment opportunities.

For example, models like HalalFi typically include Sharia screening alongside basic business verification to reduce unclear or high-risk structures.

This usually means checking whether a business is real, whether its revenue model is stable, and whether its operations align with Islamic financial principles.

The goal is to reduce guesswork for investors, not to promise guaranteed outcomes, but to improve transparency.

To understand these mechanisms in more detail, it’s usually better to review the official documentation or methodology pages provided by each platform. That helps users see how screening, profit distribution, and compliance processes are actually structured in practice.

Islamic fintech is still evolving, and different platforms experiment with different models.

Examples like HalalFi show one direction this ecosystem is moving toward: greater transparency, stronger real-economy linkage, and an effort to reduce reliance on interest-based financial structures.

Conclusion

Understanding Riba in Islam isn’t about restriction; it’s about redirection.

It’s about choosing:

Fairness over exploitation

Partnership over pressure

Purpose over profit-at-any-cost

If you’re ready to take control of your financial future, now is the time to explore halal pathways, whether through ethical investments, Islamic banking, or innovative fintech solutions.

Halalfi exists for exactly this reason: to help you grow wealth the right way, without doubt, without compromise.

Start your journey today. Because halal wealth isn’t just possible, it’s powerful.

Frequently Asked Questions

What is the difference between riba and profit?

Riba is guaranteed, risk-free gain from loans, while profit comes from trade or investment involving risk.

Can Muslims use conventional banks?

If no alternative exists, some scholars allow limited use, but the goal remains to avoid interest.

Is mortgage interest always haram?

Most scholars say yes, though some allow exceptions in non-Muslim countries under necessity.

What is the safest halal investment option?

Options like sukuk, real estate partnerships, and diversified halal funds are commonly considered safer.

How can I start avoiding Riba today?

Begin by reviewing your financial products, switching to Islamic alternatives, and educating yourself on halal finance principles.